Got Extra Income? 5 Simple Rules to Decide How Much to Save vs. Spend

A bonus, tax refund, or freelance payment can feel like breathing room. It can also disappear fast if there is no plan for it.

Financial planners say the best way to handle extra income is to split it on purpose, not by impulse. For many households dealing with higher living costs, elevated credit card rates, and uneven savings, that choice can make a real difference.

Rule 1: Cover urgent basics before anything else

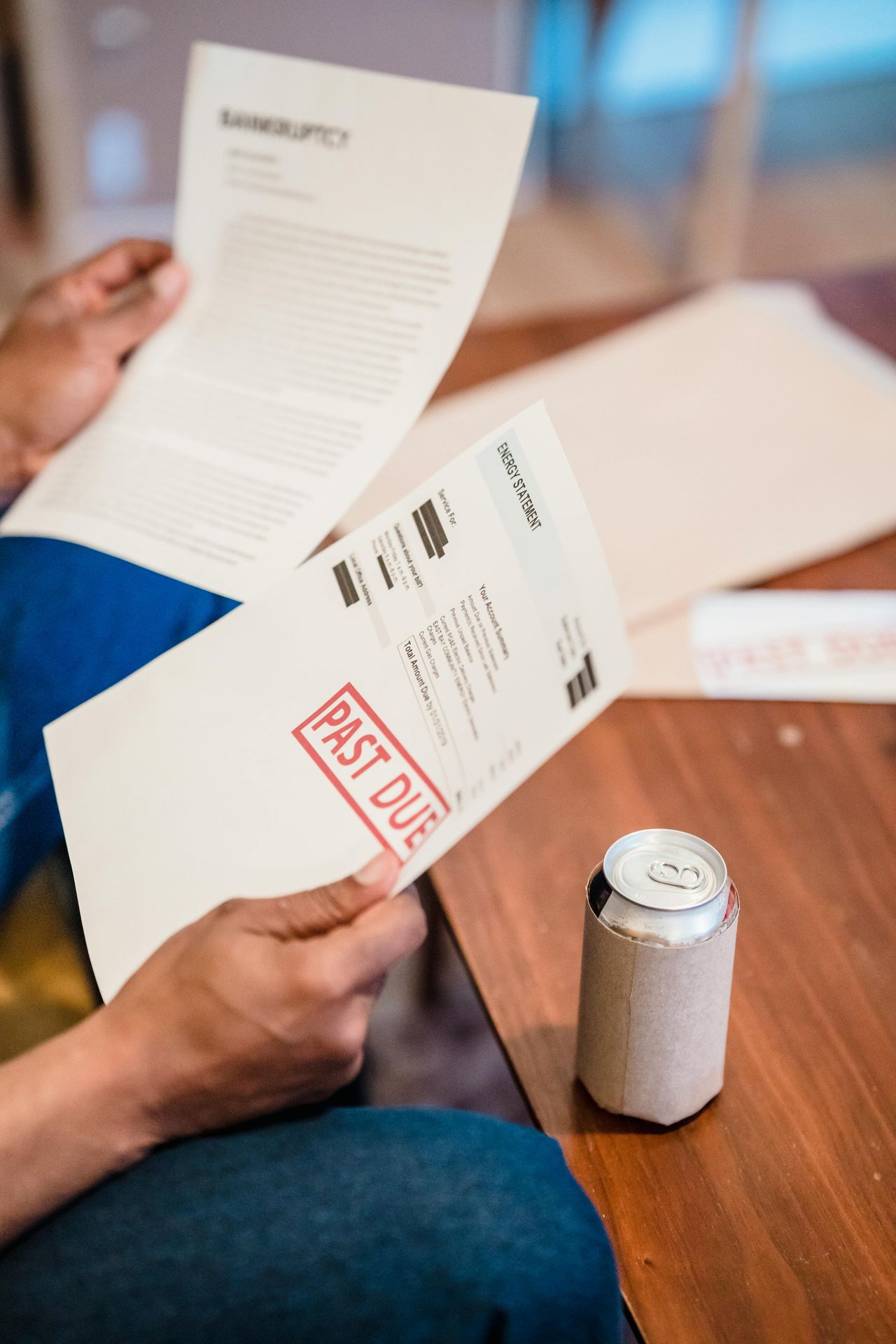

The first rule is simple: if the household is behind on bills or carrying an urgent shortfall, extra income should go there first. That includes overdue rent, utility balances, minimum debt payments, needed car repairs, or a medical bill that could trigger fees or collections. In practice, this is less about “saving versus spending” and more about stopping financial damage before it grows.

This approach reflects the reality many Americans face. Federal Reserve survey data in recent years has shown a meaningful share of adults would struggle to cover a $400 emergency with cash or its equivalent. At the same time, credit card interest rates have remained historically high, making unpaid balances much more expensive to carry month after month.

Certified financial planner Katie Brewer has often framed this as buying stability first. If extra income prevents a late fee, service shutoff, or more borrowing, it is doing important work even if it does not feel exciting. A $1,000 windfall used to catch up on essentials can have more long-term value than spreading the money across shopping, dining out, and a small savings transfer.

For readers deciding what counts as urgent, the test is straightforward. Ask what will cost more if ignored for 30 days. If the answer is rent, insurance, electricity, transportation, or a debt payment, those items move to the front of the line before any discretionary spending.

Rule 2: Keep a fixed slice for fun so the plan lasts

Experts say all-or-nothing budgeting often fails because it ignores human behavior. That is why many planners suggest setting aside a modest, fixed share of extra income for guilt-free spending. The exact amount varies, but a common range is 10% to 20%, especially when major bills are current and no acute crisis is in play.

The logic is practical, not indulgent. When people allow some room for enjoyment, they are often more likely to follow through on the rest of the plan. Behavioral economists have long noted that strict deprivation can lead to rebound spending later, where a person blows through even more money after trying to be perfect.

In real terms, that means a $500 tax refund might include $50 to $100 for something enjoyable, while the rest goes to higher-priority goals. For one household that could be dinner out and a family activity. For another, it might be replacing worn work shoes or buying a small item they have been putting off without taking on debt.

The key is setting the number before spending begins. If the fun money is decided in advance, it stays contained. If it is decided after a few impulse purchases, the extra income is more likely to vanish without improving either financial security or day-to-day quality of life.

Rule 3: Build or refill an emergency fund next

Once urgent obligations are handled, many advisers say the next stop should be emergency savings. The common starter target is $1,000, followed by 1 month of essential expenses, then eventually 3 to 6 months for households that can get there. The goal is not perfection overnight. It is creating a buffer so the next surprise does not automatically become debt.

This advice has become more relevant as households navigate persistent price pressure in groceries, insurance, housing, and auto repairs. Even when inflation has cooled from its peak, many prices remain far above pre-pandemic levels. That means small emergencies can hit harder than they did a few years ago, especially for families without spare cash.

A dedicated emergency fund also changes decision-making. Someone with even a modest reserve may be able to pay for a tire replacement, short medical visit, or emergency flight without reaching for a credit card charging more than 20% annual interest. Over time, that can reduce both stress and borrowing costs.

High-yield savings accounts have made this step somewhat more rewarding than in the low-rate years, although rates vary and can change. Still, planners generally stress that access and consistency matter more than chasing tiny differences. If extra income arrives unexpectedly, using a large share to strengthen cash reserves is often one of the safest choices available.

Rule 4: Pay down high-interest debt before making big wants a priority

If emergency savings are started or already in place, the next rule is usually to attack high-interest debt. For many Americans, that means credit card balances first, especially those carrying annual percentage rates above 20%. From a pure numbers standpoint, paying down a card charging 24% can outperform most low-risk savings options.

The effect can be larger than it appears. A household that uses $2,000 in extra income to reduce revolving credit card debt may also lower future minimum payments and free up room in the monthly budget. That gives the family more flexibility in later months, which can help prevent another cycle of borrowing for routine expenses.

This does not mean every debt should be paid off before any spending happens. Low-rate federal student loans or a fixed mortgage generally do not create the same urgency as high-rate revolving balances. The focus is on debts that are actively eroding financial progress because of steep interest and repeated compounding.

Financial counselors often recommend a clear ranking: first catch up on any critical bills, then protect against emergencies, then target the most expensive debt. If someone receives a work bonus or side-hustle payment, putting a large share toward high-interest balances may not feel glamorous. But it can create one of the fastest measurable improvements in household finances.

Rule 5: Split the rest between future goals and present life

After urgent bills, emergency savings, and costly debt are addressed, the final decision becomes easier. This is where extra income can be divided between future goals and present-day spending in a way that reflects personal values. A common rule of thumb is a 50-50 split for any remaining money, though some households prefer 70-30 in favor of saving when they are playing catch-up.

Future goals may include retirement contributions, a home down payment fund, college savings, or sinking funds for travel, holidays, and car maintenance. The advantage of assigning dollars to named goals is that it turns vague good intentions into a plan. Instead of “I should save more,” the money has a job and a timeline.

The spending side matters too. Using part of extra income on a purpose that genuinely improves daily life can be reasonable and sustainable. That could mean replacing a broken laptop needed for work, paying for child care help during a busy month, or taking a modest family outing that fits the pre-set amount.

The broader point is that extra money works best when it is divided deliberately. For most people, the right answer is not save all of it or spend all of it. It is to cover what is urgent, protect against what is next, reduce what is expensive, and then enjoy a piece of the rest without losing the bigger picture.